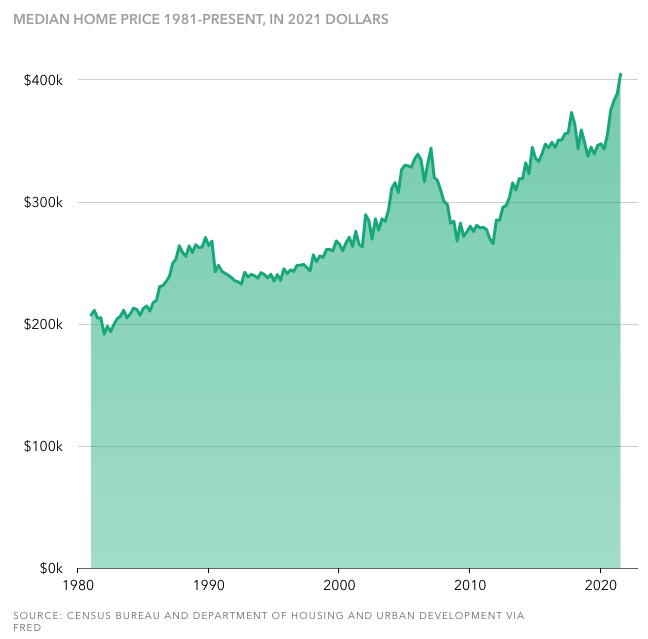

The housing market is still red-hot and current sale prices can be eye-popping. The median home price hit $405,000 in the third quarter of 2021, according to data from the Census Bureau and the Department of Housing and Urban Development. That’s up 23% from early 2020. Even before the pandemic-induced housing boom, median home prices were around $330,000.

These high prices have been a source of frustration for many young adults, who compare them to what older generations paid decades ago. These frustrations are not without merit — 40 years ago, the median home cost just $70,000.

Inflation only partially explains the difference: $70,000 in 1981 is equivalent to $205,000 in today’s dollars, roughly half of what the typical home currently costs. So houses really are much more expensive these days.

But while the houses themselves cost much more today, monthly mortgage payments are often lower than they were 40 years ago. The reason is simple: It costs less to borrow money for a home than it ever has.

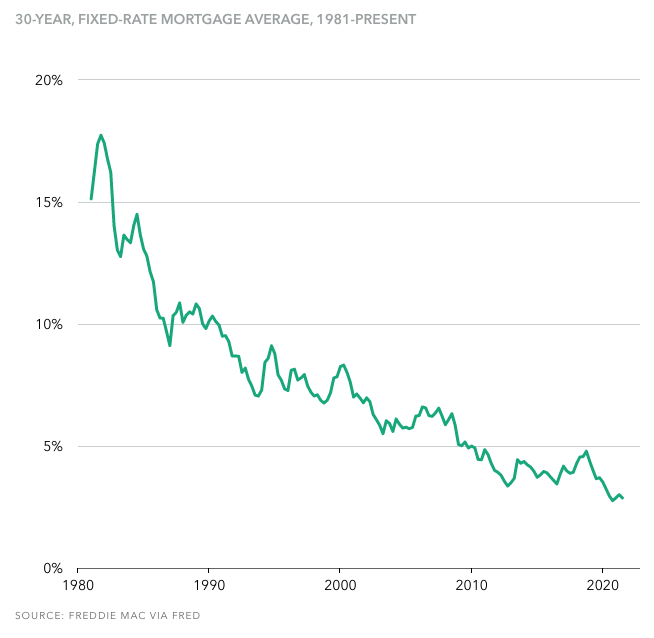

In the early 1980s, rates around 15% on a 30-year, fixed-rate mortgage were common. They have been on a downward trend ever since.

“Five percent interest rates used to be something that homebuyers cheered on when they came around, then it was fours and now it’s threes,” says Keith Gumbinger, vice president at mortgage research site HSH.com. “We really are living in favorable times. Homebuyers today have not experienced high interest rates in their adult lifetimes.”

Adjusting for inflation and interest rates adds perspective

To figure out how interest rates and home prices determine mortgage costs, Acorns calculated median monthly mortgage payments for 30-year fixed-rate mortgages over the past 40 years, based on median home prices and average mortgage rates.

The mortgage payments are hypothetical based on these calculations, and do not represent actual mortgage payments.

Here’s how lower interest rates benefit homebuyers.

Source: https://fred.stlouisfed.org/series/MSPUS

Historically, home prices have been much lower than they are today. But that didn’t always mean cheaper mortgage payments. Here’s how prices and interest rates have affected home affordability over the past 40 years. All prices are in 2021 dollars.

Source: https://fred.stlouisfed.org/series/MSPUS

In 1981, the median home sold for $205,000. Four decades later, that number has almost doubled.

Source: https://fred.stlouisfed.org/series/MORTGAGE30US

Over the same period, average rates on a 30-year fixed-rate mortgage have plummeted. In the early 1980s, rates around or above 15% were common, whereas rates under 5% have been the norm for the past decade.

Source: https://fred.stlouisfed.org/series/MORTGAGE30US

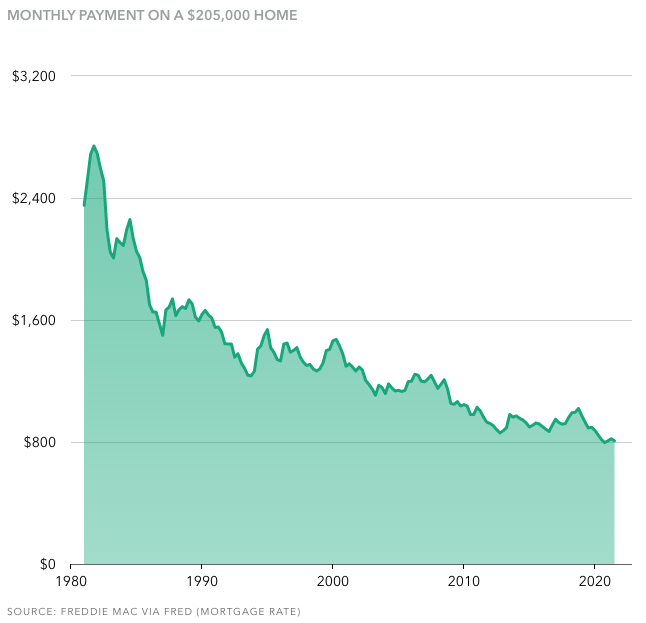

Interest rates have a dramatic effect on what people pay for their mortgages. To illustrate this, let’s look at what happens to the monthly mortgage payment for a $205,000 house when we apply the average 30-year fixed rate each year.

Source: https://fred.stlouisfed.org/series/MORTGAGE30US

Now let’s apply those rates to actual home prices. Even with rising prices, the monthly payment for a 30-year, fixed-rate mortgage on a median-priced home with a 10% down payment costs 37% less than it did 40 years ago.

Source: https://fred.stlouisfed.org/series/MORTGAGE30US

Overall, lower rates save current homebuyers hundreds of thousands of dollars in interest.

How down payments and income affect home affordability

Home prices and interest rates don’t tell the whole story. There are several other factors that determine your ability to purchase a house and what your monthly mortgage payments look like. An important one is the ability to save for a down payment. When home prices are higher, down payments are higher, too.

“Higher percent down payments were more common the further back you go,” he says, because it’s easier to save 10% of a lower home price. “If it’s a $40,000 home you only have to save up $4,000 to have a 10% down payment. If it’s a $400,000 home, that’s $40,000 of savings to come up with.”

Data before 2005 isn’t available, but Gumbinger says down payments were typically 10% or higher in the 1980s. For most of the last decade, they have hovered around 4% or 5%, according to data from Attom Data Solutions.

That’s reversing course: In the third quarter of 2021, the median down payment on a house was about 8% of the purchase price, Attom found.

Tighter mortgage guidelines and higher fees on loans that allow small down payments could be contributing to this trend, according to Attom Chief Product Officer Todd Teta. Veteran homebuyers are likely also putting down larger deposits because they’re making more money off the sales of previous homes, he says.

Coming up with a big enough down payment is a major barrier to homeownership for millennials. People born in the 1980s have 11% less wealth than previous generations did at the same period in life, according to data from the Federal Reserve Board’s 2019 Survey of Consumer Finances.

Making a lower down payment causes the monthly cost of the mortgage to go up. You’re borrowing more, and that’s a bigger principal subject to interest. With a 5% down payment on a $405,000 house instead of 10%, the monthly mortgage goes from $1,511 to $1,595.

A lower down payment could mean a higher interest rate. Lenders consider these loans to be riskier, and they will often charge higher interest rates to compensate.

It’s also important to consider incomes when looking at historical home prices, says Gumbinger. While home prices have doubled since 1981, median household income has risen 27% since 1984, the earliest year data is available.

Combined with lower interest rates, this means monthly mortgage payments are actually more affordable today. A monthly mortgage payment of $1,511 represents 27% of the median household income, compared to 48% for the median mortgage payment in 1984.

Getting the best interest rate you can is key

While 30-year, fixed-rate mortgages are the dominant product on the market today, throughout the past 40 years, adjustable-rate mortgages, 40-year mortgages, and other products rose in popularity as an alternative to high rates on 30-year, fixed-rate mortgages. In the late 1990s and early 2000s, for instance, adjustable-rate mortgages represented as many as 35% of mortgage applications, compared to just 3% today.

First-time homebuyers today “have really only known a fixed-rate environment,” says Gumbinger. “They’ve also only known a very favorable interest rate environment.”

In the end, getting the best rate you can on a mortgage will help you buy a home, even when prices are high. Boosting your credit score can help you qualify for a better rate. You can save hundreds of dollars per month and thousands over the life of your mortgage with a score of 760 or above.

This material has been presented for informational and educational purposes only. The views expressed in the articles above are generalized and may not be appropriate for all investors. The information contained in this article should not be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product. There is no guarantee that past performance will recur or result in a positive outcome. Carefully consider your financial situation, including investment objective, time horizon, risk tolerance, and fees prior to making any investment decisions. No level of diversification or asset allocation can ensure profits or guarantee against losses. Article contributors are not affiliated with Acorns Advisers, LLC. and do not provide investment advice to Acorns’ clients. Acorns is not engaged in rendering tax, legal or accounting advice. Please consult a qualified professional for this type of service.

Kiersten Schmidt was the graphics editor for Grow.